We are not the first to note the profound impact that COVID-19 has had on global supply chains. More recently, the Russian invasion of Ukraine has further tested and weakened this global network and placed even greater emphasis on the requirement for supply chain resilience. But resilience comes at a cost, and whilst ‘just in case’ may currently be preferred over ‘just in time’, the pressures to optimize use of cash and working capital have not gone away. With its exposure to global supply chains, the European specialty chemicals sector is one such industry that has been materially affected by these emerging challenges and conflicting pressures.

Our 2021/22 European Specialty Chemicals Survey identifies that price stability of raw materials, reliability of supply volume and on-time performance remain the chief supply chain-related concerns within the sector. Further, players are significantly stepping up efforts to increase security of materials by diversifying supply chains and are seeking to take less risk in pricing through their commercial contracting.

These are among the key findings of L.E.K. Consulting’s 2021/22 European Specialty Chemicals Study, a survey of 207 chemical sector professionals across a broad range of industries and functions. Our survey included leaders and senior decision-makers in France, Germany, Italy, Spain and the United Kingdom.

Read on to hear more about what they told us.

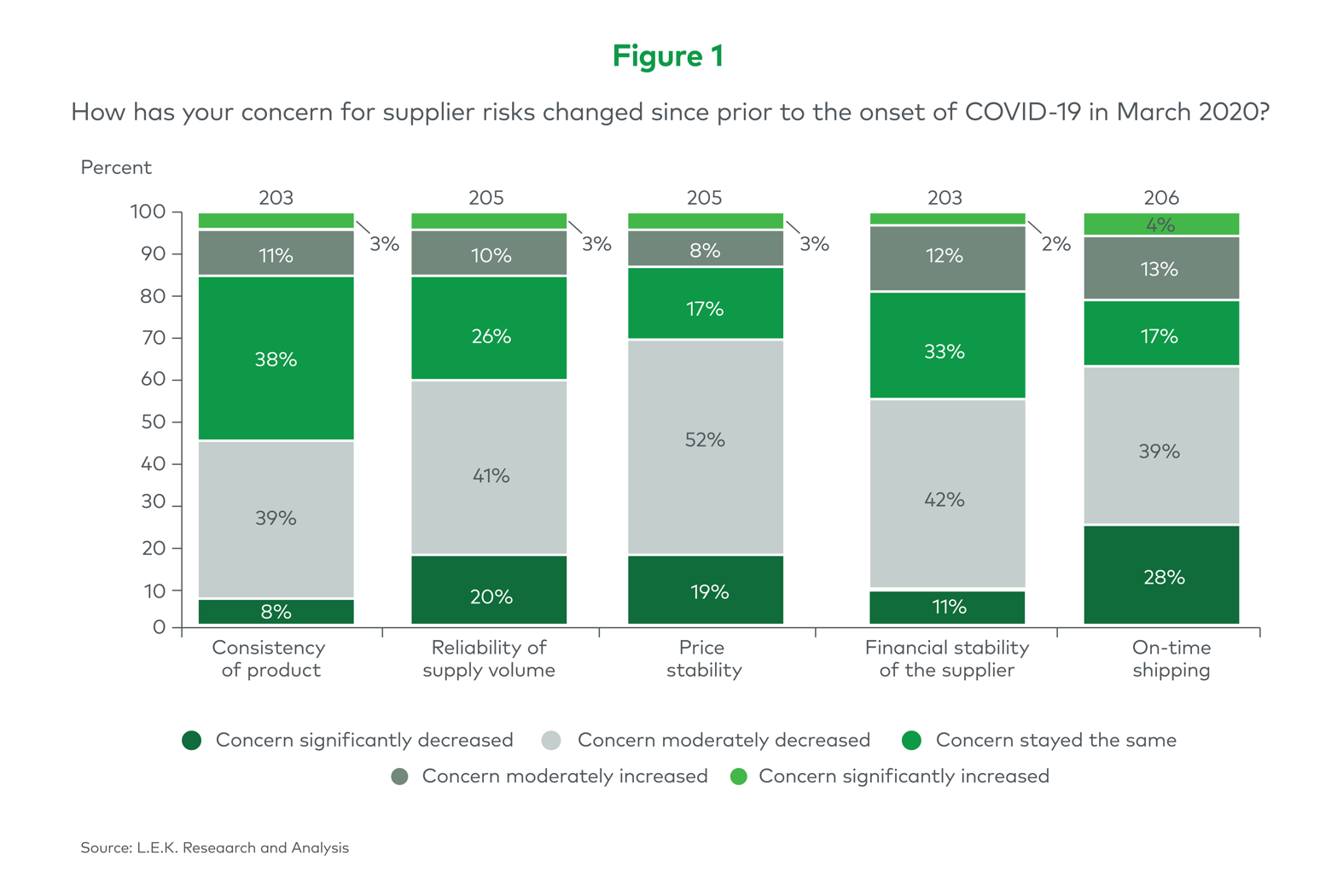

Price stability and reliability of supply are the chief supply chain concerns for the specialty chemicals sector

When asked to relay how their sentiment had changed in the past 18 months with respect to five specific supply chain areas, across all regions our panel reported significant increases in their level of concern: in particular, on-time shipping, reliability in supply volumes and the pricing stability of raw materials (see Figure 1):

-

Respondents from the United Kingdom reported the greatest increases in concern in reliability of supply volumes, perhaps because of the combined supply chain challenges associated with COVID-19 and Brexit

-

Conversely, across each of France, Italy, Germany and Spain, the number one area of increased concern was pricing stability

In more recent months, these supply chain challenges are likely only to have increased. The global rise in inflationary pressure continues to affect pricing stability. In addition, Russia’s invasion of Ukraine continues to have far-reaching consequences for European supply chains in this sector, particularly given Russia’s historically high levels of chemical exports.

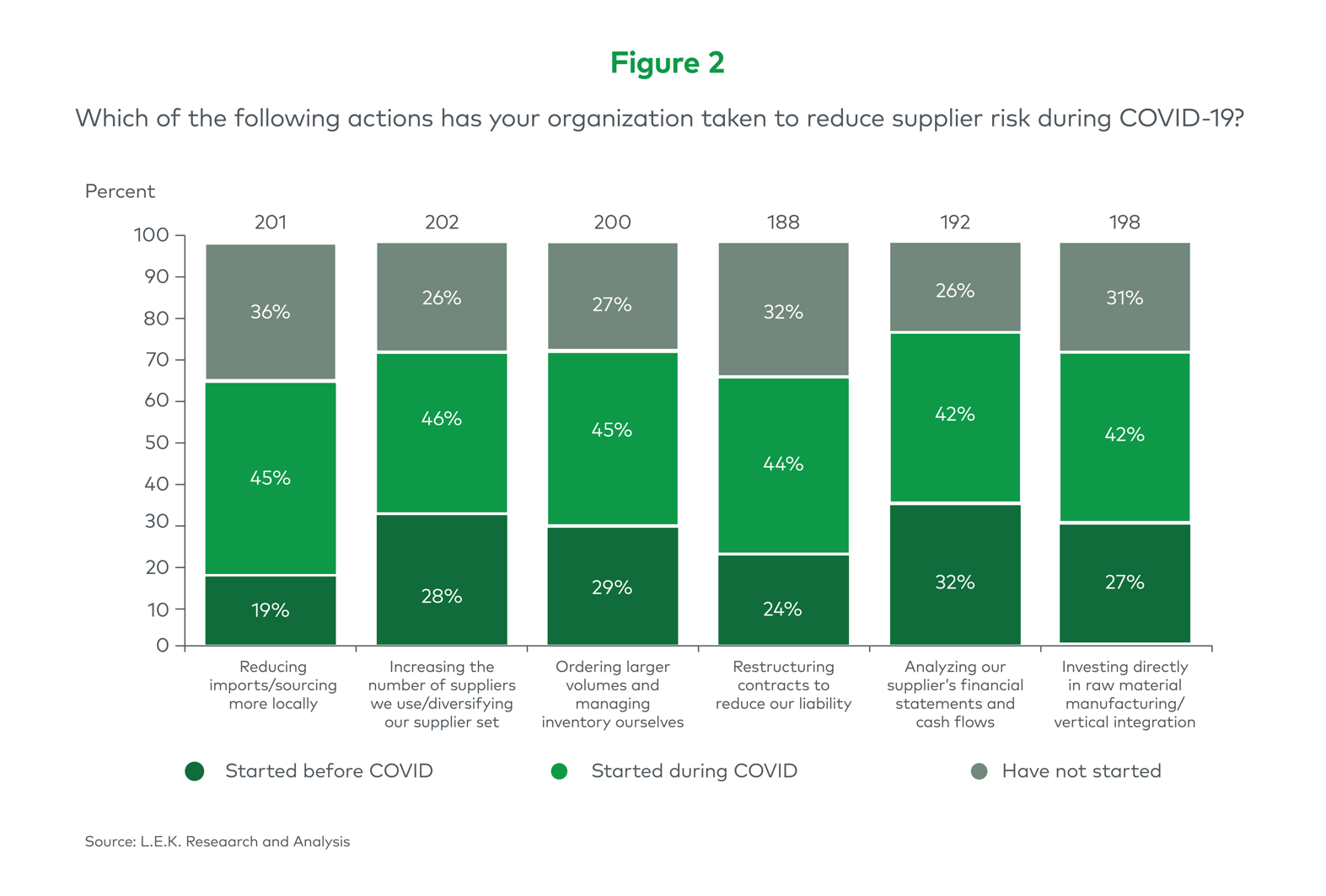

The specialty chemicals sector is addressing these challenges through a broad set of resilience measures

In response to these challenges, there has been a step change in activity to build supply chain resilience. European specialty chemicals companies are taking a variety of actions, including diversifying their suppliers, increasing inventory levels, sourcing more raw materials locally, reducing commercial contract risk, analyzing the financial stability of their suppliers and increasing their vertical integration. Across the board, our panel reported a 40%+ increase in adoption of each of these new initiatives, specifically to reduce supplier risk (see Figure 2).

A significant proportion of our panel (45%) reported that they have increased order volumes, and consequently moderated inventory levels upwards to mitigate risk. This indicates a shift in preference from lean supply chain management towards a more cash-intensive, but more resilient, approach.

Companies are also taking a more proactive approach to managing their commercial risk in their contracting structures. Relative to pre-COVID-19 levels, there has been a significant increase (>2.5x) in companies reporting that they are looking to restructure their contracts to redistribute supply chain risk in their favour. Our UK respondents reported a particularly high increase in this activity, with 84% of survey respondents reporting that they were restructuring contracts to reduce price risk exposure, compared to just 18% before the pandemic. Relatedly, and across the full panel, respondents reported a significantly higher (42%) level of interest in financial due diligence being performed on key suppliers.

Finally, our panel indicated that there has been a marked effort to reduce reliance on imports, and to increase levels of local sourcing following the COVID-19 pandemic; the proportion of respondents who showed interest in localising their supply chains increased from just 19% to 64% over the COVID-19 period — a greater than threefold increase. Some respondents indicate a willingness to go further. Since COVID-19, 42% of the panel reported that they have started investing directly in raw material manufacturing and deeper vertical integration as a means of resolving supply chain challenges.

Looking to the future

Which of these changes will be here to stay?

Many of the changes implemented by our panel — such as decisions to order in larger quantities and raise inventory levels — reflect tactical, short-term shifts in approach. As and when confidence in supply chains returns, the pressures of cash flow optimization will continue to exert downwards pressure on inventory levels and may cause a return to leaner management. However, other changes — such as deepening vertical integration and increasing reliance on local supply relative to imports — reflect more structural shifts to supply chain management which may be significantly longer lasting.

We hope you have enjoyed discovering the findings of L.E.K.’s 2021/22 European Specialty Chemicals Survey on supply chain risks and would invite you to click here to find out more about our global chemicals business.

01062023110122