Packaging Volumes Are Set To Rise, but Pricing Pressures Remain Challenging

The demand trends driving brand owners’ packaging decisions: Part 1 of a three-article series on the 2024 European Brand Owner Packaging Survey

The demand trends driving brand owners’ packaging decisions: Part 1 of a three-article series on the 2024 European Brand Owner Packaging Survey

One of the key conclusions of our latest European survey on packaging is that the participants are looking forward to a surge in demand for packaging, driven by both volume and value.

With around 90% of the brand owners we spoke to across Europe expecting higher consumer demand and increased inventory levels in 2024, we note an end to recent destocking trends. Along with growing demand, our survey indicates an increase in spending fueled by pricing pressures. With these powerful factors at play, it’s little wonder that we registered plenty of confidence from those who took part in our survey.

As ever, the devil is in the details, and our annual proprietary packaging survey — conducted during December 2023 and January 2024 — delves deeper into the demand trends that will shape brand owners’ packaging decisions.

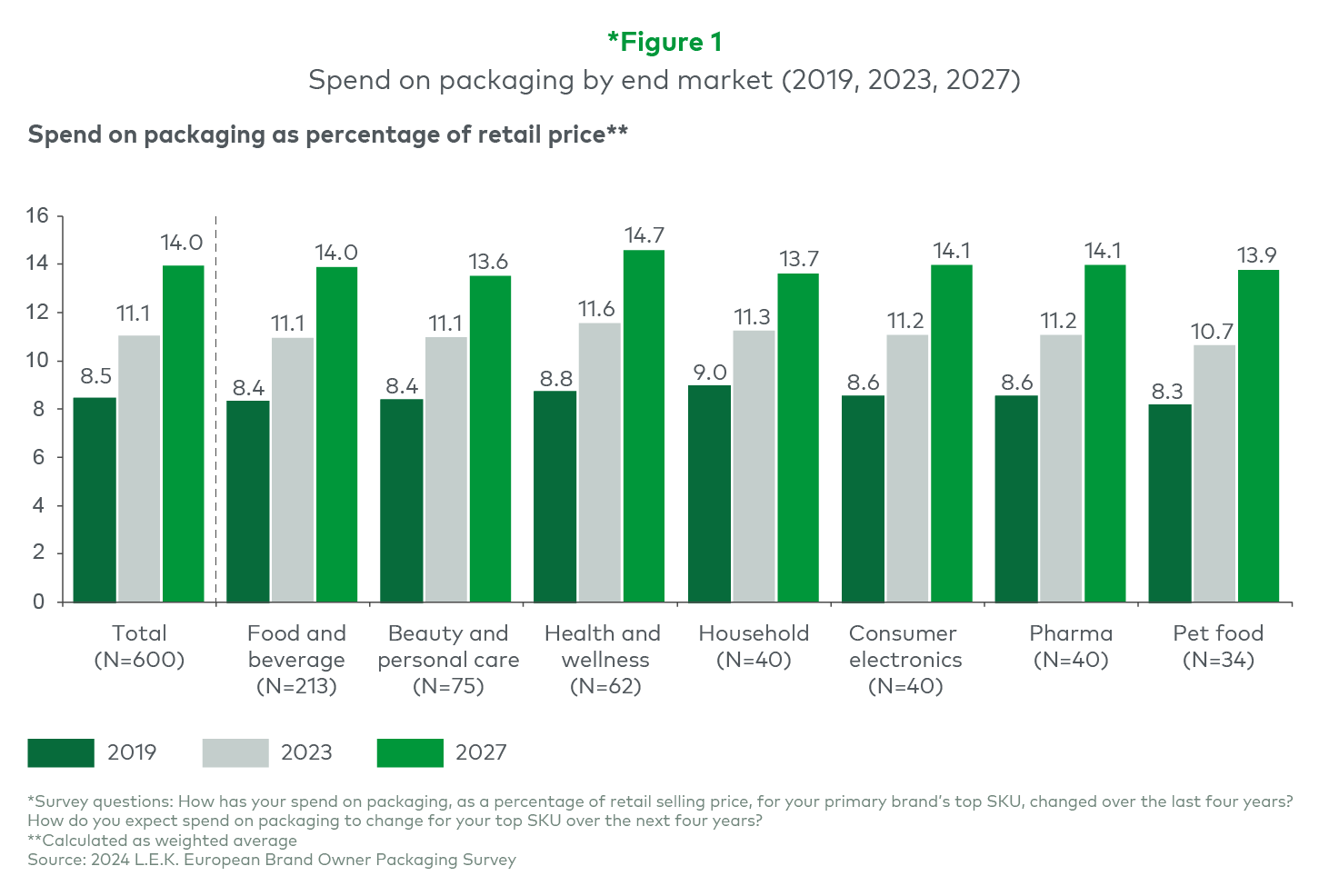

Jumping from about 9% to approximately 11% between 2019 and 2023 and expected to hit around 14% by 2027, packaging spend as a share of retail selling price is increasing throughout Europe.

What’s driving this trend? Our survey reveals a potent combination of both volume and pricing dynamics, encouraging European brand owners to up their investment in packaging.

Across all countries, brand owners expect to see an uptick in inventory levels for 2023-24, implying higher volumes. They also report an increase in packaging prices relative to retail selling prices. This shift in pricing dynamics is most keenly felt in the health and wellness categories categories (see Figure 1).

Consumer demand and SKU count are both on the rise and expected to drive up demand for packaging in the year ahead.

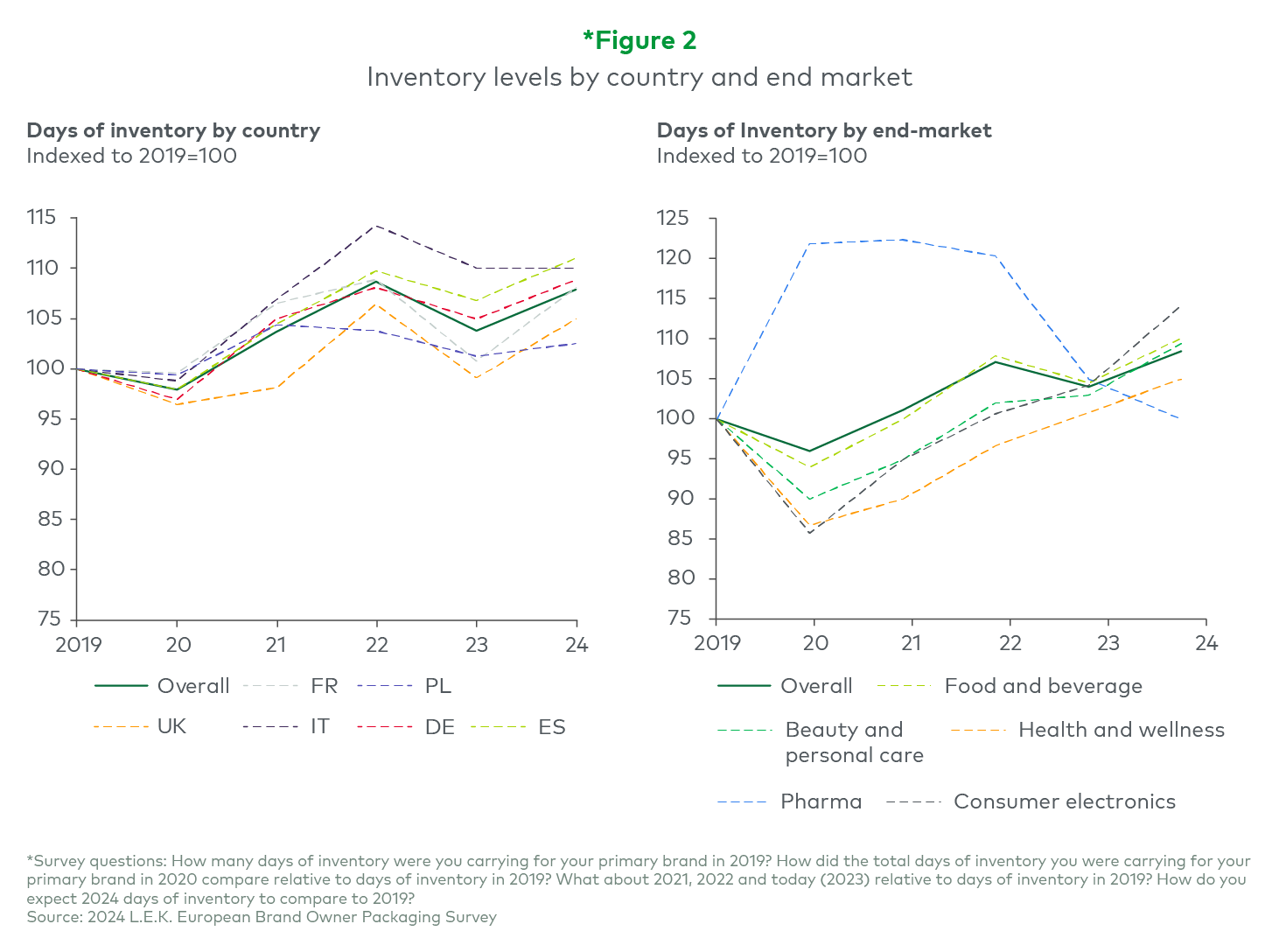

The destocking trends of 2023 appear to have run their course and inventory levels have increased since 2019 and look set to rise during 2024. Figure 2 shows how inventory levels have fluctuated during the past five years, with 2020’s dip driven by supply chain issues as stocks ran low. 2023 saw an overall drop in inventory levels, primarily attributed to de-stocking trends as supply chain challenges subside. 2024’s renewed uptick in inventory levels is largely driven by an increase in the types of products in demand and a drop in pressure on cost reduction from inventory carrying costs.

While stocking and destocking timelines have been remarkably similar across countries, the UK stands out for its ongoing supply chain disruptions into 2021, and Poland exhibited the most stable performance.

Stocking and destocking trends have varied across different end markets. The health and wellness and consumer electronics sectors experienced the greatest decline in inventory levels as households adjusted their spending during pandemic lockdowns. In contrast, the pharmaceutical sector saw increased stock levels in the early stages of the pandemic due to uncertainty. By 2023, all end markets have generally returned to pre-pandemic conditions of 2019. Recently, heightened geopolitical instability has affected trade capacity and increased transport times as containers are rerouted around the Red Sea. This has significantly impacted freight rates for goods primarily shipped from Asia, such as consumer electronics, compared to more locally sourced end markets like food & beverage.

It’s good news for European packaging suppliers, as brands are expecting to increasingly source packaging from within the EU, a decision driven by both superior supplier performance and increased responsiveness to short-term needs.

While many of the brand owners we canvassed reported some ability to pass on cost increases to their customers, mounting pressure on margins driven by the recent period of high inflation remains a persistent issue. On average, about 13% of packaging costs were passed on, and respondents believe that consumers will bear a further 4% before any notable decline in sales. As usual, this varied across categories, with consumer electronics topping the table with approximately 15% already passed on and a further 5% expected, while cannabis at about 11% of costs passed on and another 4% expected to trail.

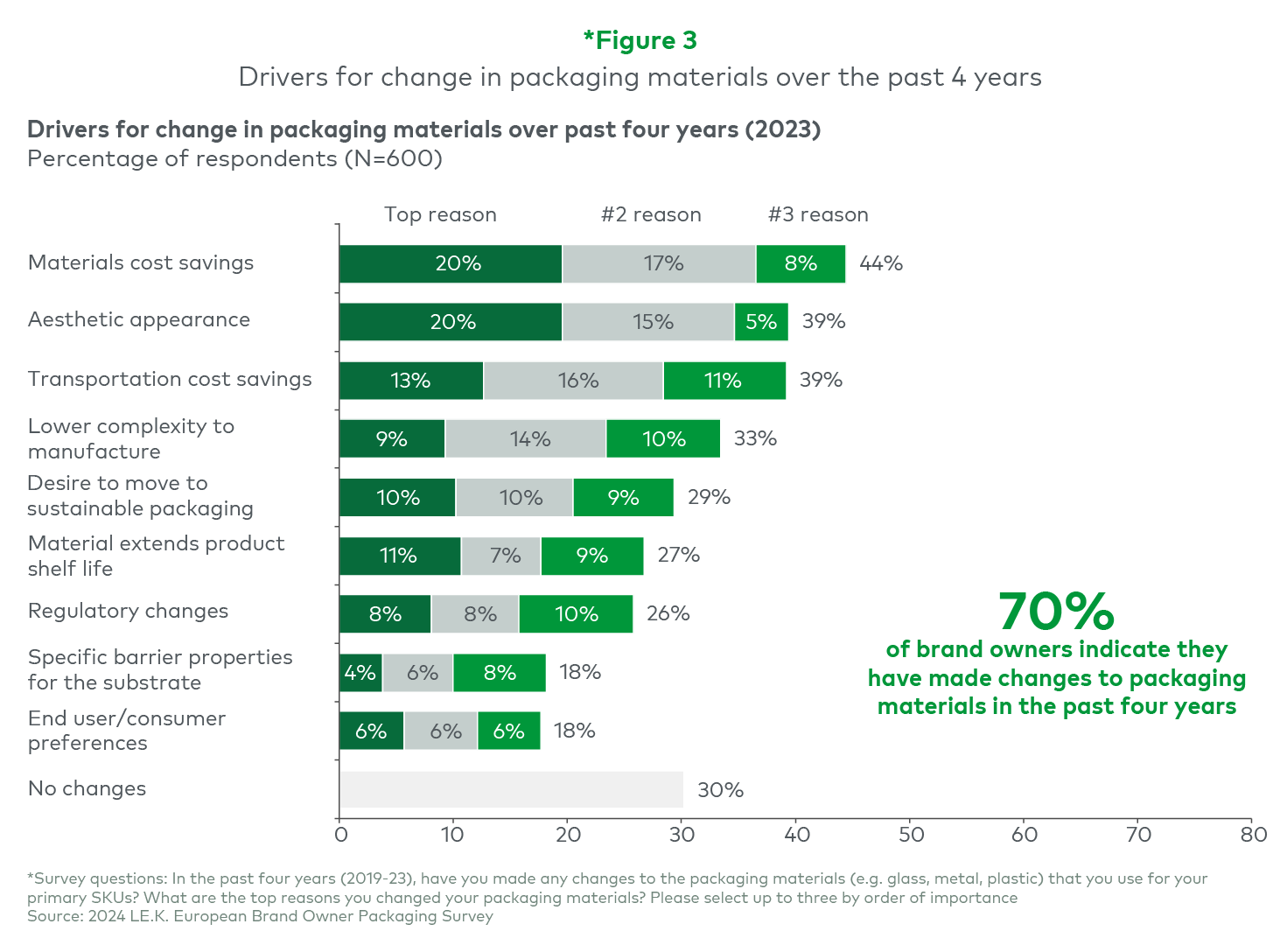

In marked contrast to our 2022 survey findings, when sustainability was seen as the key driver for change, this year’s big emphasis on material cost savings appears to be a direct response to the prevailing inflationary macroeconomic conditions (see Figure 3). Resourceful brand owners are looking to switch to lower-cost packaging materials and cheaper transportation alternatives as a way to preserve margins and retain profitability. While sustainability remains important, it is now considered alongside other objectives, reflecting a shift in priorities as revealed by our survey.

In our next article we look at how investment and innovation fared in our survey findings, and our third article covers sustainability in more detail. To talk to us about these topics or to access the full survey results, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting