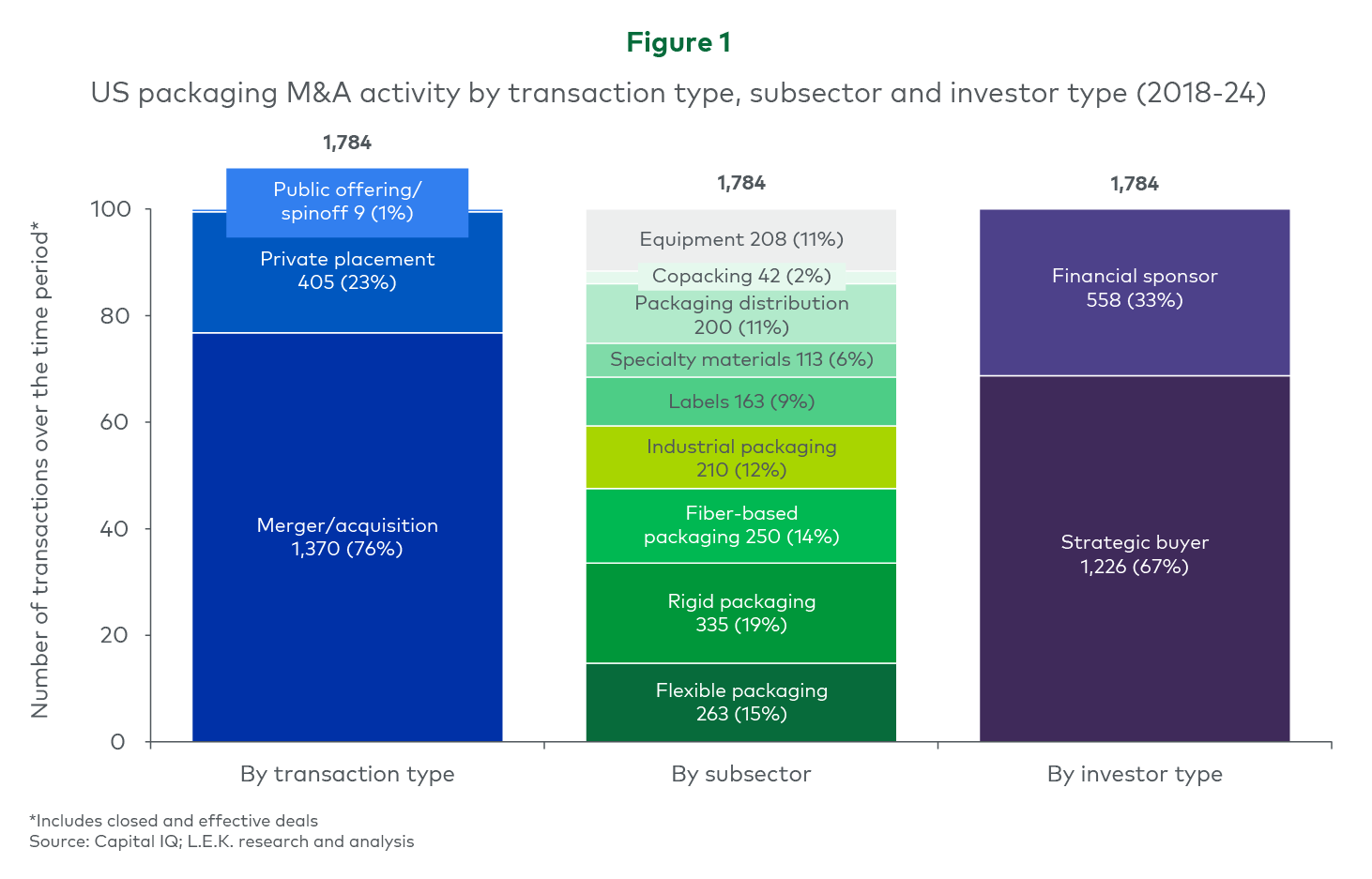

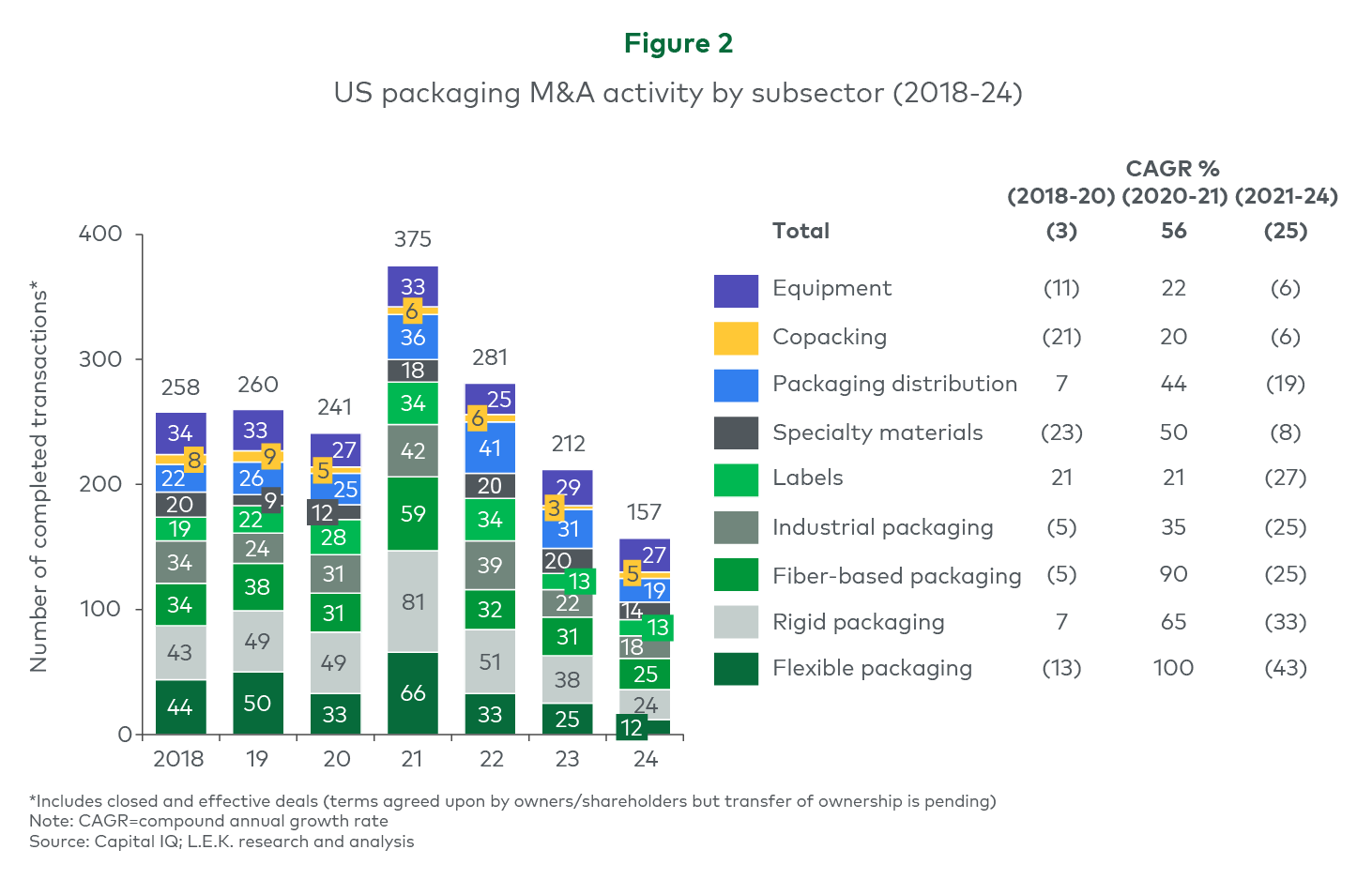

Nearly 1,800 packaging transactions closed between 2018 and 2024, with strong diversification across the broader packaging ecosystem (e.g., flexibles, rigid, specialty materials, equipment) (see Figure 1). However, this period saw tremendous volatility. Transaction volume peaked in 2021 (56% p.a. growth 2020-21) and then declined materially across subcategories between 2021 and 2024 (25% p.a. decline).

Since mid-2022, the packaging sector has experienced a dearth of activity, leading to pent-up supply of longer-held assets and unfilled demand from buyers looking for exposure in the sector. In this article, L.E.K. Consulting examines transaction volume trends across 2018-24 to help inform the shape of the recovery and the future of packaging M&A, including which segments could recover sooner rather than later, as well as the broader implications for both buyers and sellers.

3-year cooling period after 2021 activity spike

Due to favorable macroeconomic factors (e.g., abundant low capital costs) and tailwinds within the packaging sector (e.g., strong packaging volume growth in the early days of the COVID-19 pandemic, cycle resistance), packaging transaction volume reached a peak in 2021, capping off seven years of historically high transaction numbers. Transaction volume then slowed substantially across packaging subsectors between 2021 and 2024, declining ~25% per annum because of rising interest rates, inflation, sales volume drops associated with consumer wallet softness, and the extension of pandemic-driven destocking hold periods (see Figure 2).

Transaction volumes within both the flexible and the rigid packaging segments experienced significant growth from 2020 to 2021, comprising ~40% of transaction volume due to high levels of fragmentation in the market and diverse products/end uses (e.g., food, household goods, medical), creating abundant M&A opportunities. These same segments then experienced the steepest decline in transaction volume from 2021 to 2024 (see Figure 2).

Strategic buyers to remain dominant in driving consolidation

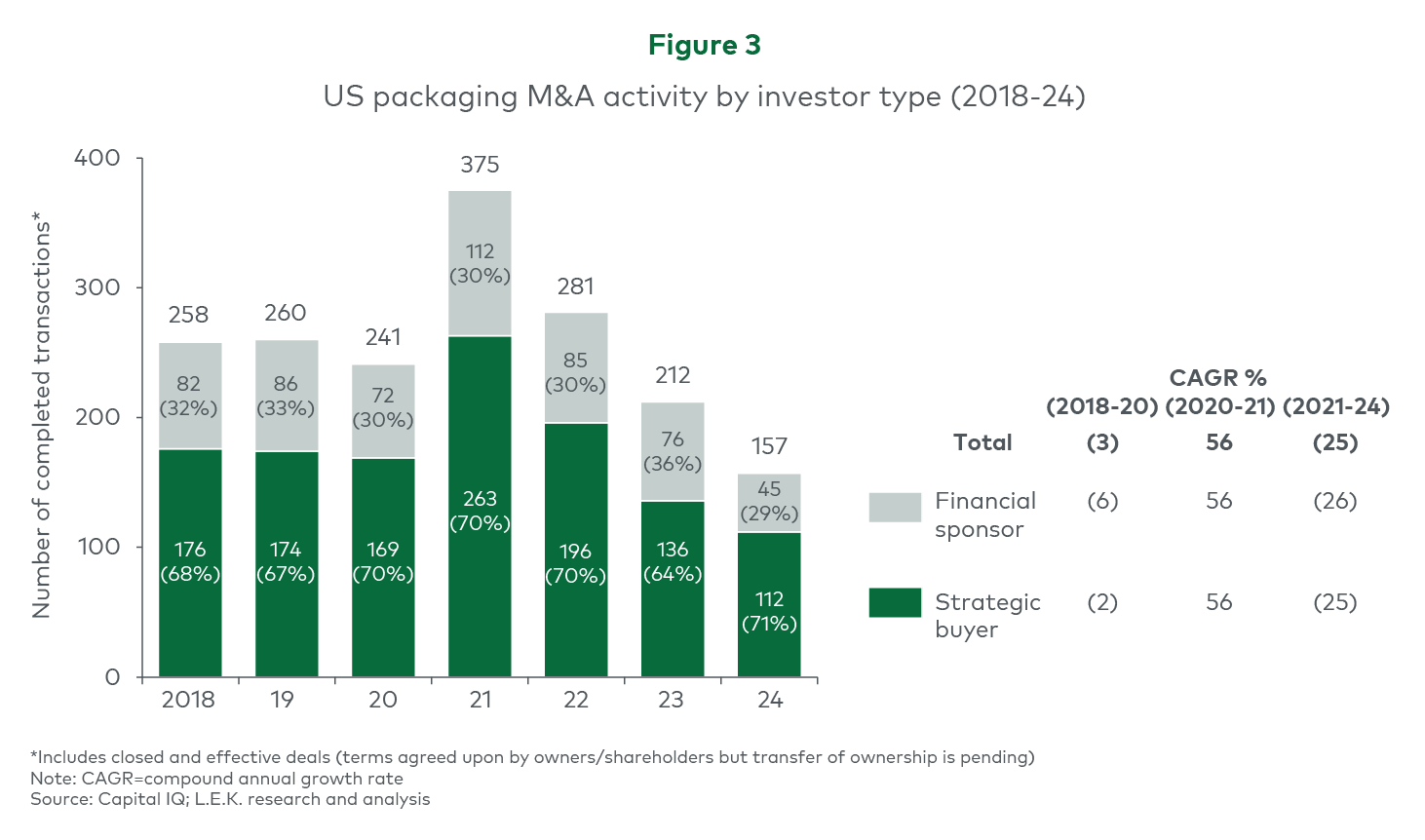

Strategic buyers (including sponsor-owned platforms) have been the most active investors (~67% of total M&A volume during 2018-24) in the packaging sector, reflecting a continued trend of consolidation as players look to build scaled, more-efficient platforms across geographies, end markets and product portfolios (see Figure 1).

We expect strategic buyers to remain dominant in driving consolidation and M&A activity despite an approximately 25% per annum decline in strategic acquisitions between 2021 and 2024, which was caused largely by major players’ reevaluations of their portfolios as they worked to streamline operations and focus on core competencies (see Figure 3). This shift has been exacerbated by the increased cost of capital and buyers’ and sellers’ difficulties with aligning on deal terms (e.g., multiples paid).

Going forward, strategic buyers are expected to take a more cautious approach to M&A as they assess their businesses’ capital needs and benchmark M&A opportunities against other forms of investment.

Depth of assets awaiting subsequent transactions

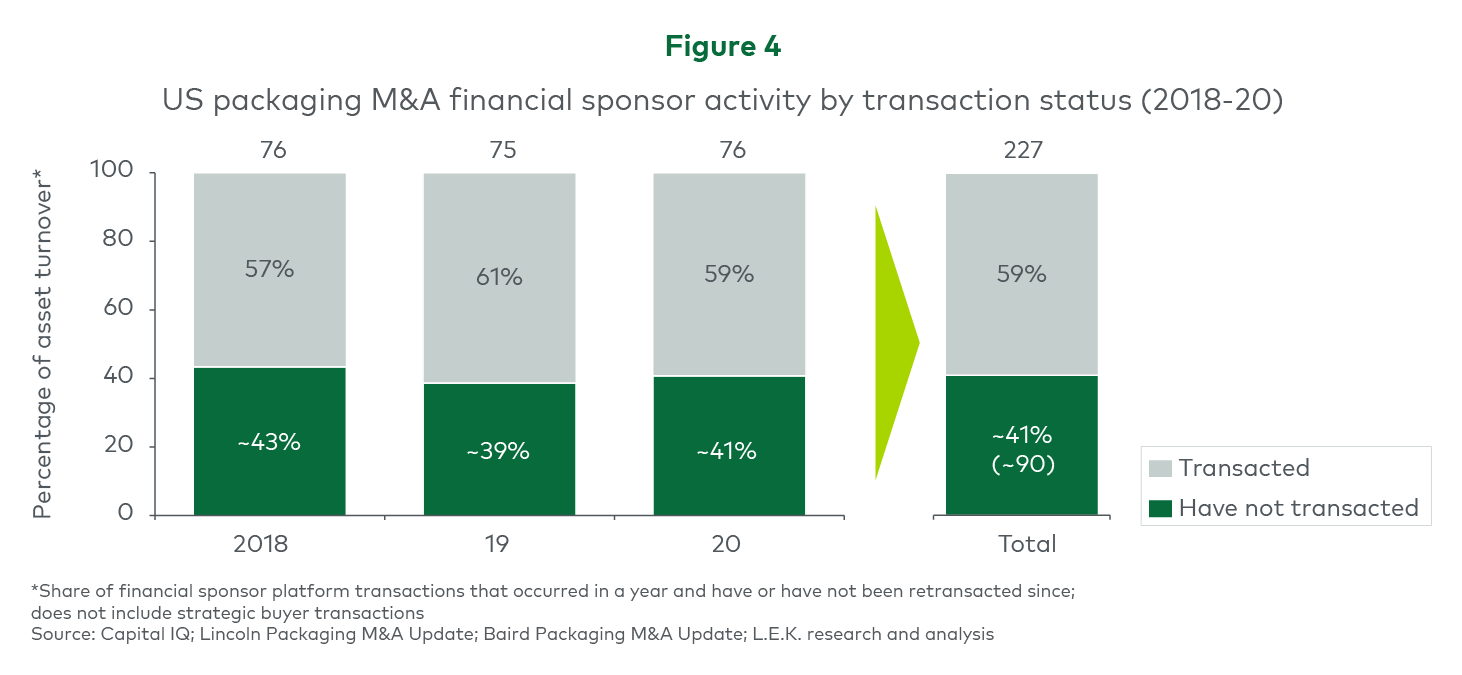

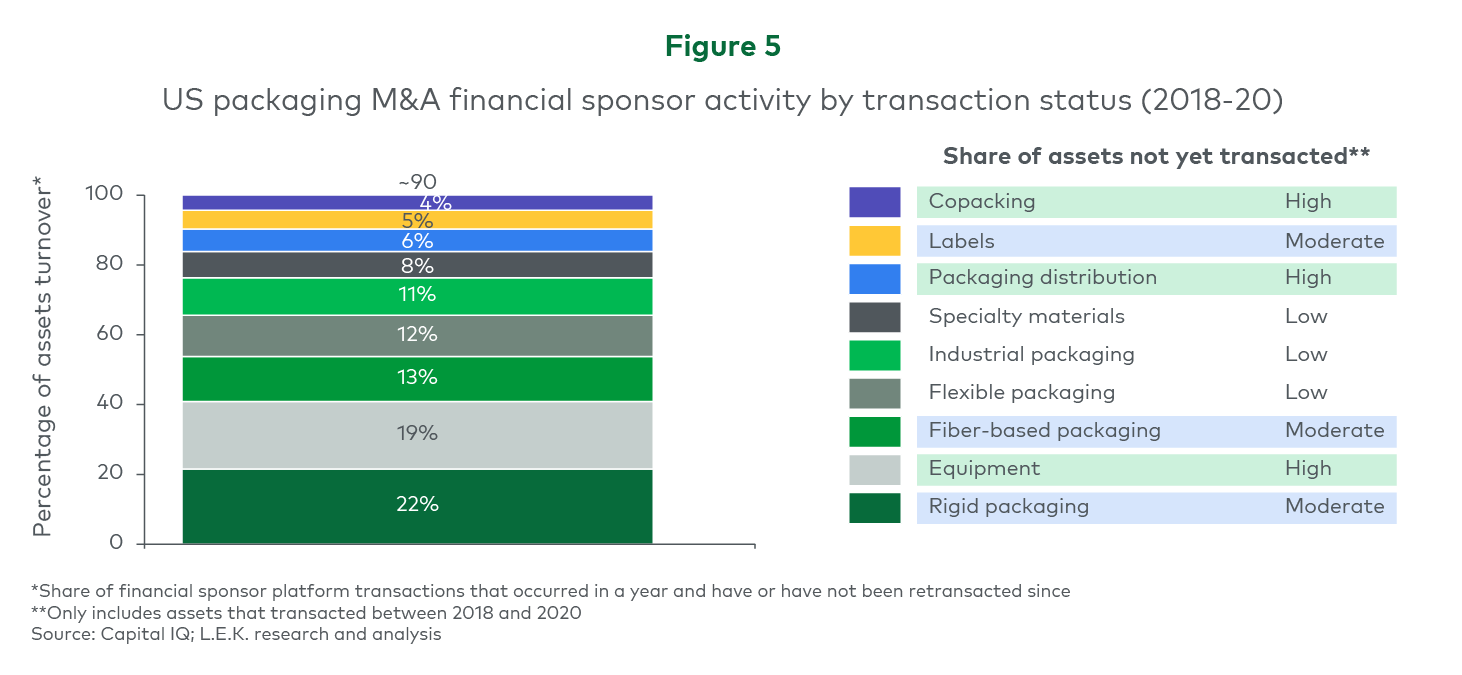

Financial sponsors hold a robust portfolio of assets that were acquired between 2018 and 2020 but have not subsequently transacted. In fact, approximately 41% of packaging assets that transacted to a financial sponsor between 2018 and 2020 have not subsequently transacted (see Figure 4).

Meanwhile, the equipment, packaging distribution and co-packing segments have the highest shares of assets that have not transacted (see Figure 5).

These assets are now likely approaching the end of their hold periods, many of which were extended, as mentioned earlier, due to COVID-19, macroeconomic conditions (e.g., rising interest rates, inflation), destocking and volume challenges from lowered consumer confidence.

Industry participants involved in packaging M&A are more optimistic about transaction activity in the near term compared to 2024, as packaging volume challenges associated with destocking dynamics come to an end and consumer spending begins to trend toward normal following elevated inflation. However, key factors will likely impact what assets come to market and ultimately transact in the near term.

Although distribution of assets across subsectors is fairly even, assets more heavily impacted by destocking (i.e., those serving more shelf-stable product categories within food, beverage, home and personal care) could take longer to come to market as sellers continue to delay transactions in order to show normalized EBITDA levels and volume growth for their businesses.

Conclusion

Looking toward 2025 and beyond, there are solid reasons for optimism among sellers wanting to realize a return on a previous investment and buyers wishing to gain or increase exposure in the packaging sector.

Although many sellers are hopeful that their business assets have returned to normal, strategic buyers remain interested in platform-building, and more favorable macroeconomic conditions should boost sellers’ confidence in their ability to successfully transact. Buyers are likely to find an increased supply of available assets across segments. This should expand the probability that they will find assets to align well with their investment goals.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

04042025100407