Industrial equipment and technology executives in the U.S. are facing a raft of challenges, from inflation and tariffs to supply chain disruption, demand planning and backlog concerns — all against a backdrop of broader economic uncertainty.

High inflation and ongoing tariff threats have led to increased material costs and pricing in industrial manufacturing. Supply shocks and the prioritization of onshoring combined with the potential of a pro-U.S. manufacturing policy have created a volatile supply-and-demand environment. Accurately forecasting demand levels to capacity has never been more important.

But as L.E.K. Consulting’s survey of executives at 200 U.S. blue chip manufacturing organizations found, their longer-term sentiment on achieving strategic goals remains quite optimistic.

Conducted in March 2025, the latest annual version of the survey was designed to uncover not just how these industry leaders — whose titles include chief commercial officer, head of strategic development, VP of integrated offerings and VP of strategic sales — are addressing the myriad challenges currently facing their organizations, but how, in the midst of those challenges, they are planning for the future.

What we found was that while many of the executives’ priorities remain the same as in years past, the relative importance of those priorities has shifted along with their focus.

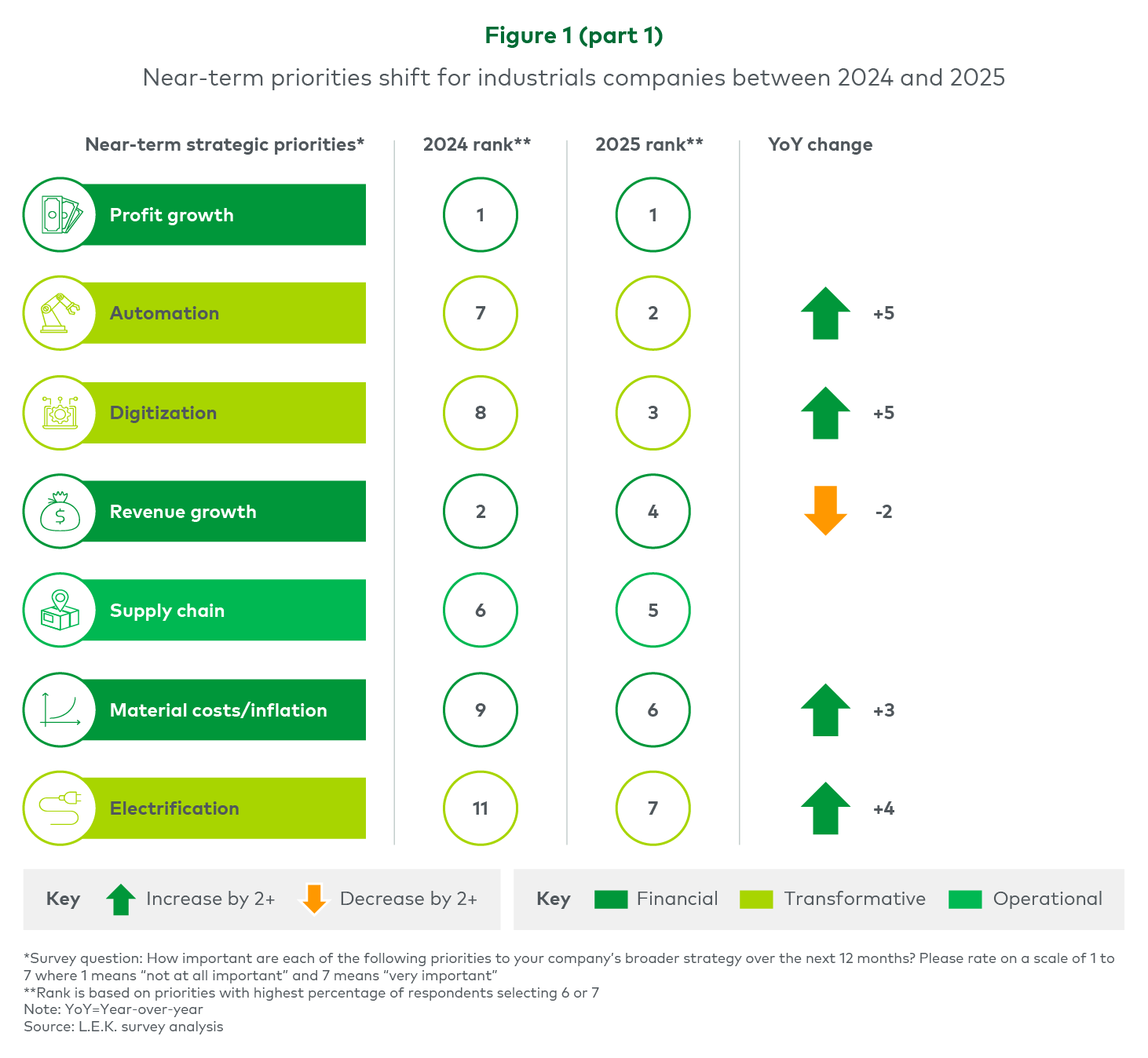

Focus returns to profitability

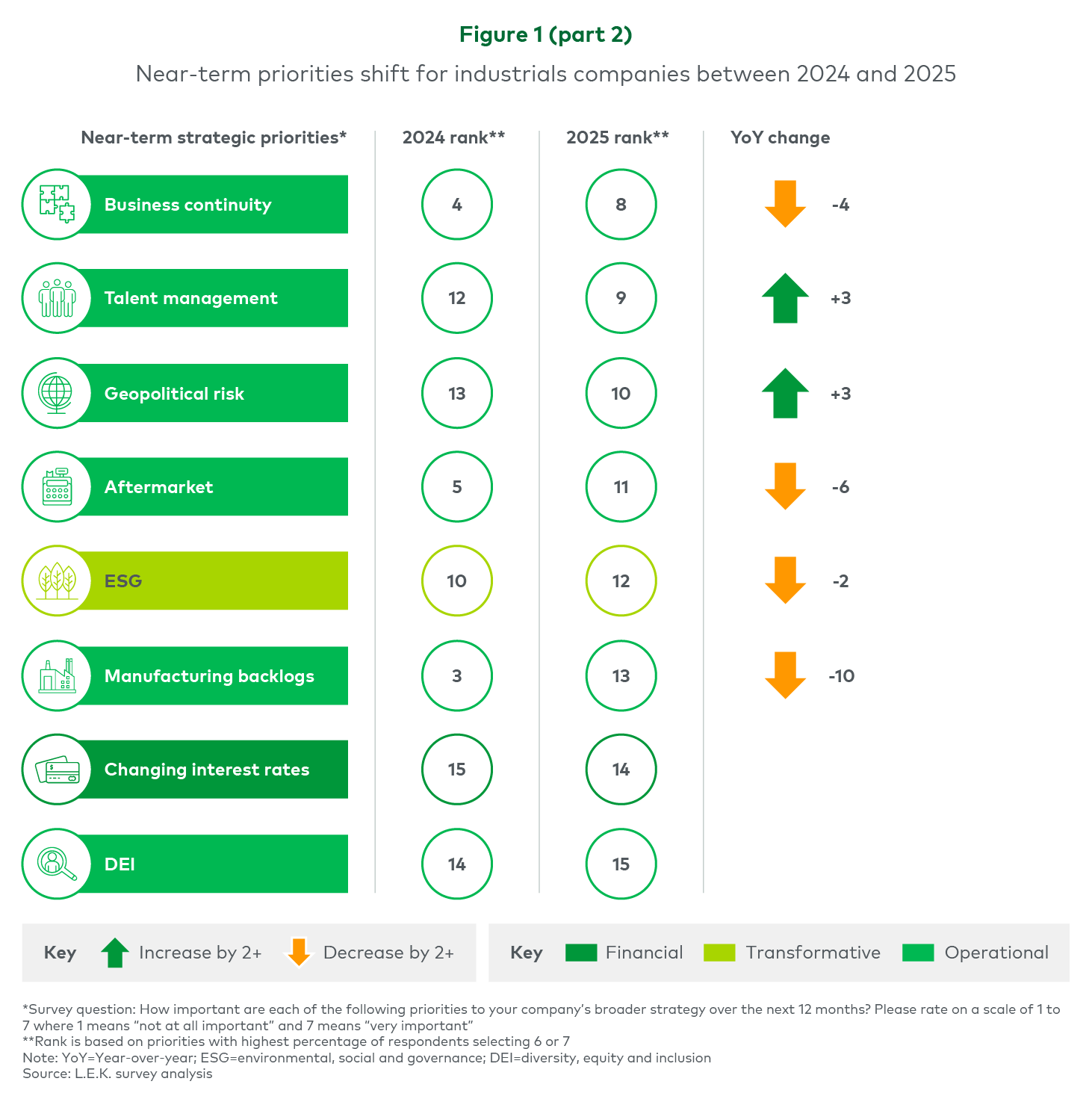

As these leading industrial technology manufacturer decision-makers make clear, profit and efficiency are, once again, their top priorities. Profit growth remains the top near-term priority, with margin-expanding initiatives such as automation and digitization making significant leaps in this year’s top-three list. Meanwhile, manufacturing backlogs, which were a top priority last year, have since largely moved out of focus (see Figure 1, parts 1 and 2).

To achieve their strategic goals, U.S. industrial firms are pursuing profit growth, automation and digitization and are doing so by prioritizing higher-margin products, aiming for eventual transformation to full automation and leveraging technology to improve their organizations’ operations, respectively.

Substantive trade/tariff plans still to come

When it comes to developing meaningful tariff/trade war plans, industrial executives are in “wait and see” mode. To be sure, mitigating negative impacts from tariffs and trade controls/sanctions are among their top concerns in the near term. But they’re holding off on putting in place more time-intensive/costly initiatives like relocating manufacturing and shifting supply chains until the longer-term outlook — and any related implications — becomes clearer and are implementing, no-regrets but albeit lower-impact actions instead.

Our survey respondents are most concerned about potential negative impacts from changes to tariffs and export controls, and among potential trade policy changes see tariffs as the most likely to be implemented. Indeed, in the weeks following the deployment of our survey, the Trump administration rolled out sweeping tariffs to many trade partner countries, justifying industrial companies’ concerns.

In the meantime, the most common actions being taken by manufacturing firms to prepare for tariffs are exploring new supplier relationships and reviewing price strategies.

Optimism about achieving future goals

Despite challenges in meeting immediate-term goals, industrial executives remain confident and optimistic in their ability to progress against goals in the medium and longer term and so are putting their focus there.

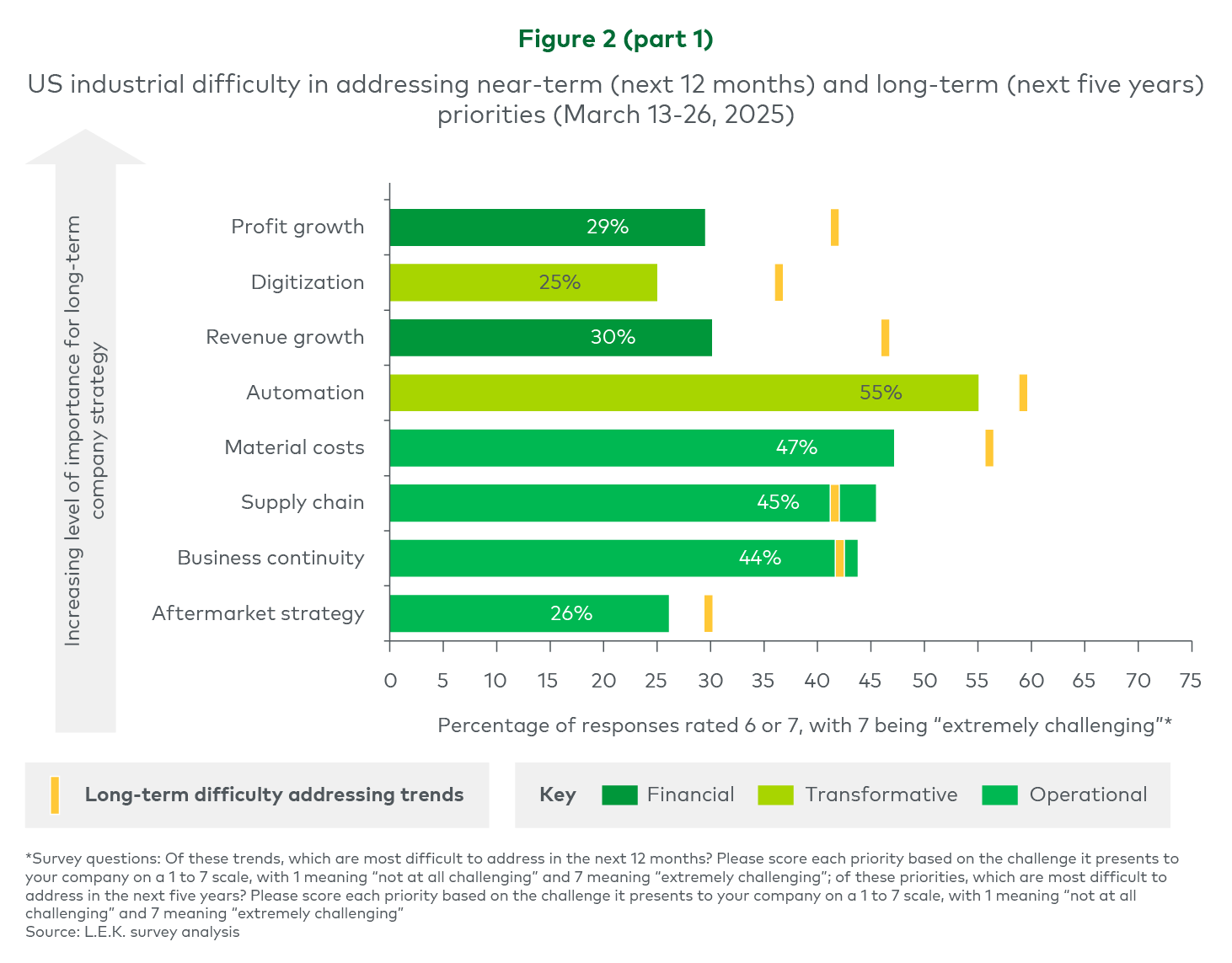

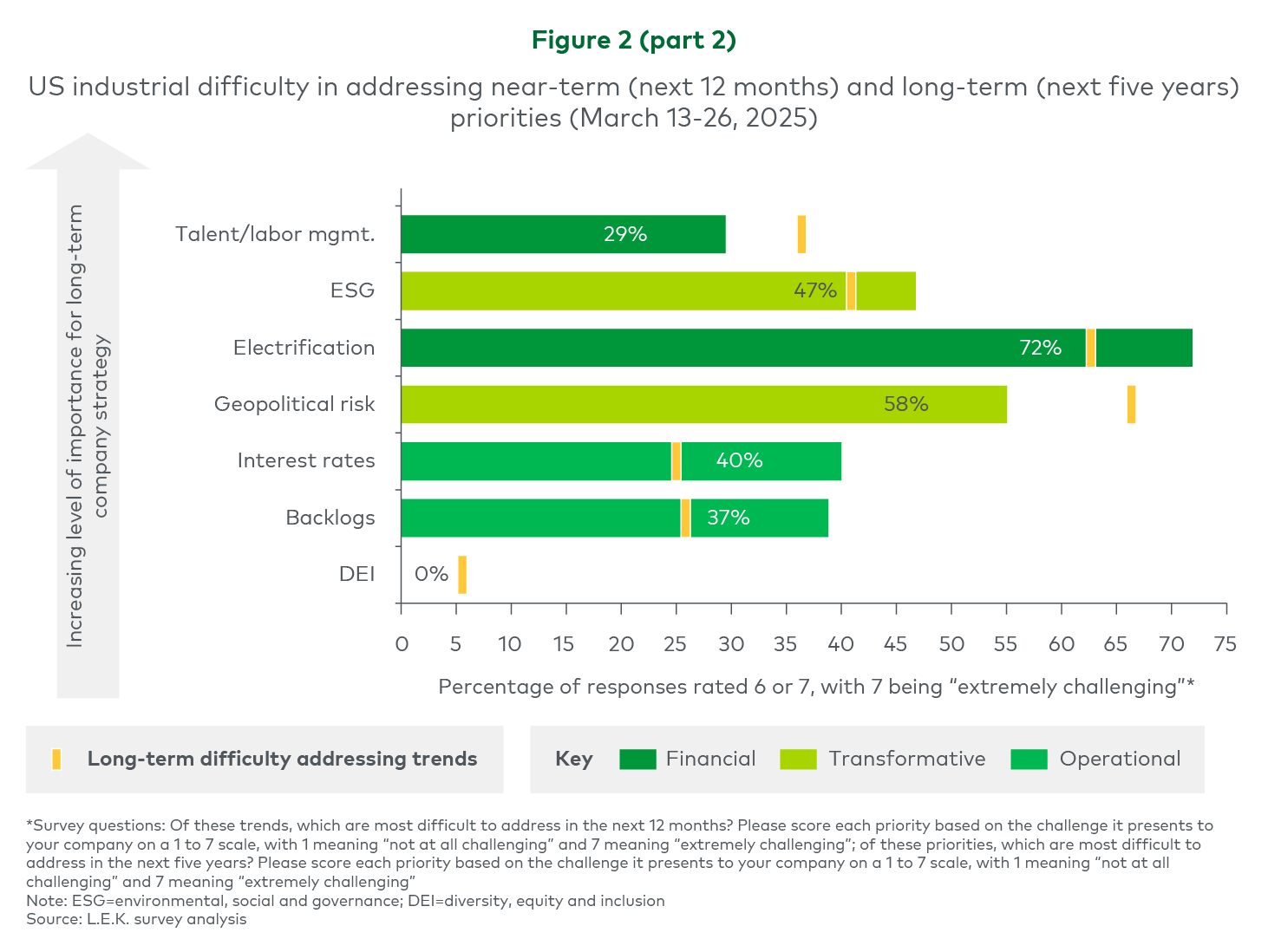

In the short term (i.e., the next 12 months), industrial companies are focusing on financial goals as well as digitization and automation, with other high-priority issues like supply chain and material costs slightly lagging. In the long term (i.e., the next five years), industrial companies have prioritized executing against their profitability and revenue goals.

Meanwhile, when it comes to automation and digitization, a greater proportion of firms appear to still be in the planning phase. Unsurprisingly, given that longer-term priorities often require more-involved planning and nuanced execution, U.S. industrial companies generally view them as more difficult to address (see Figure 2, parts 1 and 2).

Still early innings for digital solutions

Many industrial companies are expanding their use of digital solutions, with enterprise apps, customer data solutions and cybersecurity measures the most widely adopted so far. And the executives we surveyed expect such expansion to continue going forward.

That’s especially true when it comes to the adoption of generative artificial intelligence (AI). Industrial executives recognize the technology’s broad applicability to business functions and processes and plan to advance their implementation of it to increase efficiency. While most companies believe they are realizing significant value from AI, they are likely only utilizing a small-to-moderate proportion of the full functionality.

Digital solutions serve a wide range of business purposes, with some — such as customer data solutions for customer experience — being more tailored to specific initiatives and others serving broader applications. Increasing efficiency is the highest priority for AI usage among current users, while increasing competitiveness and expanding revenue streams rank lower in priority. But these are likely to grow in focus as manufacturing companies become more comfortable with implementing AI and stepping up their use of advanced functionality.

With a shifting landscape comes shifting priorities

As our latest survey of industrial equipment and technology executives makes clear, financial priorities, particularly profit growth, remain key for executives.

That said, in light of the relative demand softness, revenue growth appears to have been slightly deprioritized in the near term relative to potential efficiency-boosting measures such as automation and digitization.

As one of our survey respondents put it, “As a manufacturing firm, the bottom line is always what you’re evaluated on. Top-line growth is always nice, but in this environment, everyone is really focusing on driving profitability.” Meanwhile, material costs/inflation have also become a more significant focus as executives await clarity on impending tariffs and other potential trade policy changes.

Industrial executives remain optimistic. But they know the ground is shifting beneath them, and until that shifting stops or at least slows down, they’re going to proceed with caution.

Those are the high-level themes that our survey of industrial manufacturing executives reveals. For a more granular picture, be sure to read our deep dives into the areas that those executives have made their top priorities: procurement and the supply chain, services and the aftermarket, pricing, electrification, and technology, notably automation and digitization.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

08222025130818