The cost-of-living crisis has left an indelible mark on UK consumer behaviour, but as inflation concerns continue to recede, retailers, brand owners and investors are keen to understand how spending habits are likely to evolve as household budgets improve. This article recaps the areas where consumers have tightened their belts and sheds light on where consumers are currently expected to prioritise spending whilst the economic climate recovers.

The state of consumer sentiment

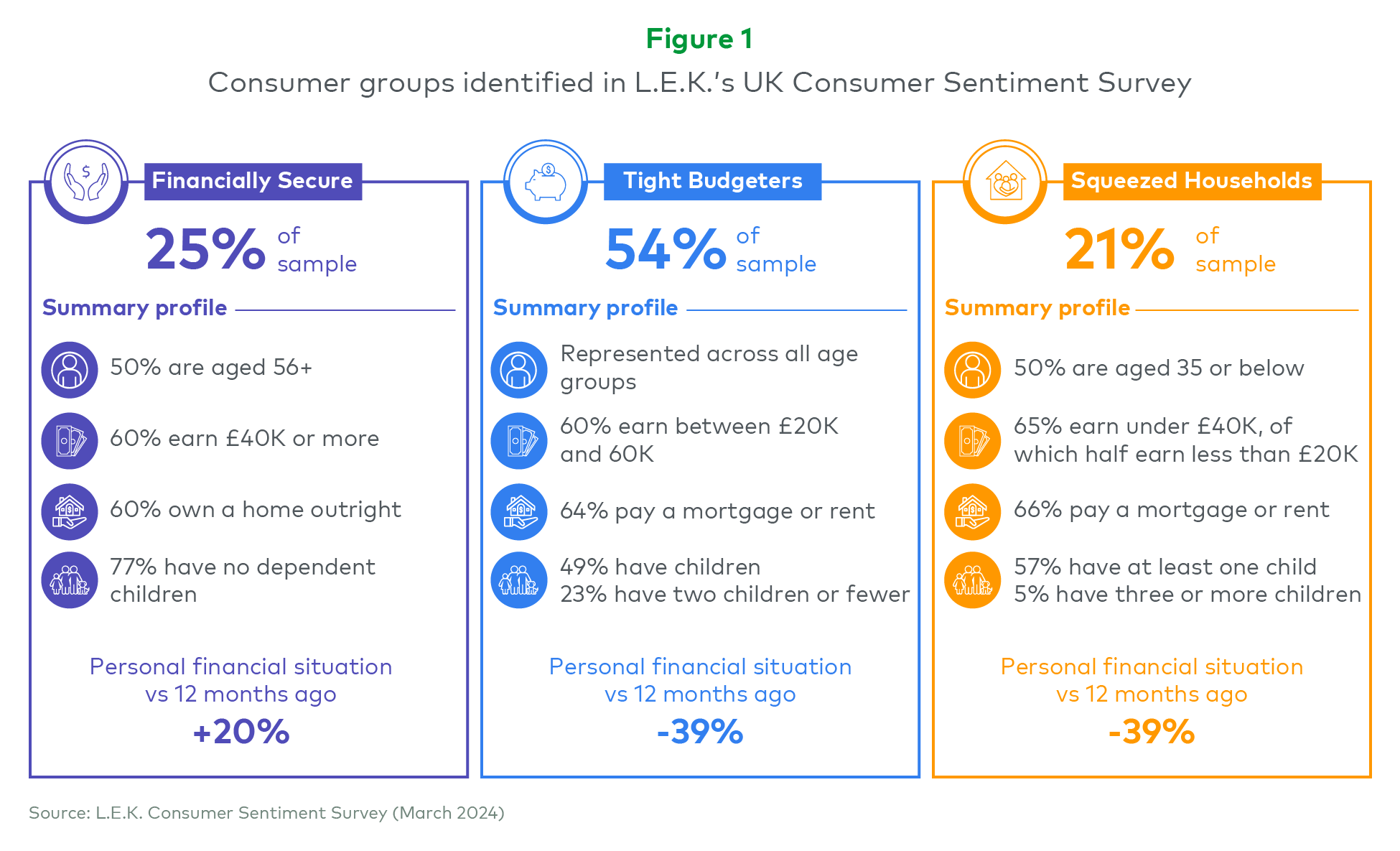

L.E.K. Consulting has been tracking consumer sentiment and behaviour throughout the cost-of-living crisis. Our most recent survey* reveals a cautiously optimistic picture. While consumer confidence is on the mend, overall sentiment remains muted. Some consumers reported improvement in their personal finances (19% feeling better about personal finances compared with the previous year), but others expressed ongoing concerns about, for example, energy costs, inflation, mortgage rates/rent and personal debt.

The survey identified three primary consumer groups (see Figure 1):

- Financially Secure

- Tight Budgeters

- Squeezed Households

Each group exhibited distinct characteristics in terms of income levels, home ownership and financial responsibilities. These groups offer a glimpse into how different segments of the population have had to manage their budget and make spending trade-offs and indeed how different segments of the UK population may respond as the economy recovers.

Better news ahead for discretionary spending

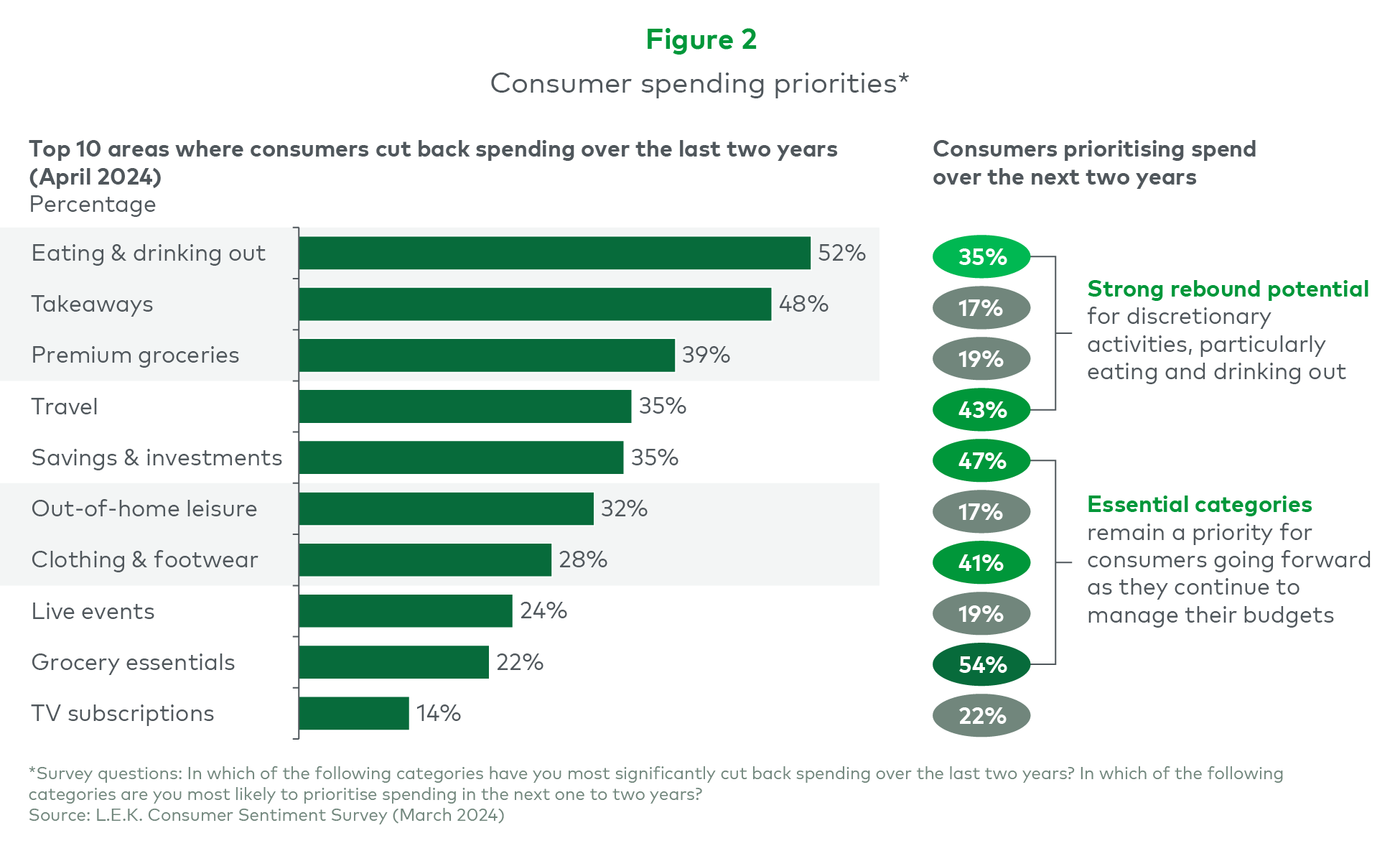

One of the most noticeable trends is the shift in discretionary spending. Over the past two years, consumers have necessarily had to cut back on indulgences, but as household budgets begin to rebuild, our survey identified a renewed interest in spending on non-essential items like dining out and clothing. We’ve identified some headline trends in spending, looking back and looking forward (see Figure 2). Travel is expected to remain a priority, as it has been through the Covid-19 recovery, alongside grocery essentials.

Grocery market trends

The data highlights that recent shifts within the grocery market towards value and own-label products, as well as more deliberate shopping for some household items at value-oriented grocers, will continue beyond the cost-of-living crisis, showcasing a trend towards prioritising affordability and value in spending decisions. This is true across all of the consumer groups, with 72% of the Financially Secure respondents and 74% of Squeezed Households indicating that they will stick to own-label products even with increased budgets. These entrenched behaviours will mean footfall spanning most customer segments remains well-distributed across mainstream and value-oriented grocers. As a result, brands (and investors) will have to actively drive distribution strategies throughout the landscape and remain vigilant about price positioning and brand marketing to maximise relevance across channels/retailers.

Respondents also pointed to a desire to reprioritise fresh food — particularly fruit and vegetables (60% of total respondents) — as grocery budgets rebuild. This is likely to play out through mainstream grocery outlets and specialised retailers (e.g. butchers and bakeries). Within non-fresh groceries, categories that remain convenient and good value for money, like frozen foods, are expected to remain popular, with almost 30% of Squeezed Households viewing them as a priority.

Health and wellness trends

Personal well-being continues to be a priority for UK consumers. More than 80% of consumers across all segments have maintained spend on vitamins and supplements over the last two years, building on Covid-19-linked momentum, and more than 40% of both Tight Budgeters and Squeezed Households plan to increase spend on vitamins and supplements when household budgets allow.

Key areas of interest in the market include digestive health (probiotics, gut health, etc.) and women’s health.

Skincare and haircare also remain priority areas within consumers’ personal healthcare spending.

Beauty services is another area expected to benefit with the improvement of the economic climate, with 49% of female respondents indicating they would have more beauty treatments if they had 10%-20% more to spend in this area.

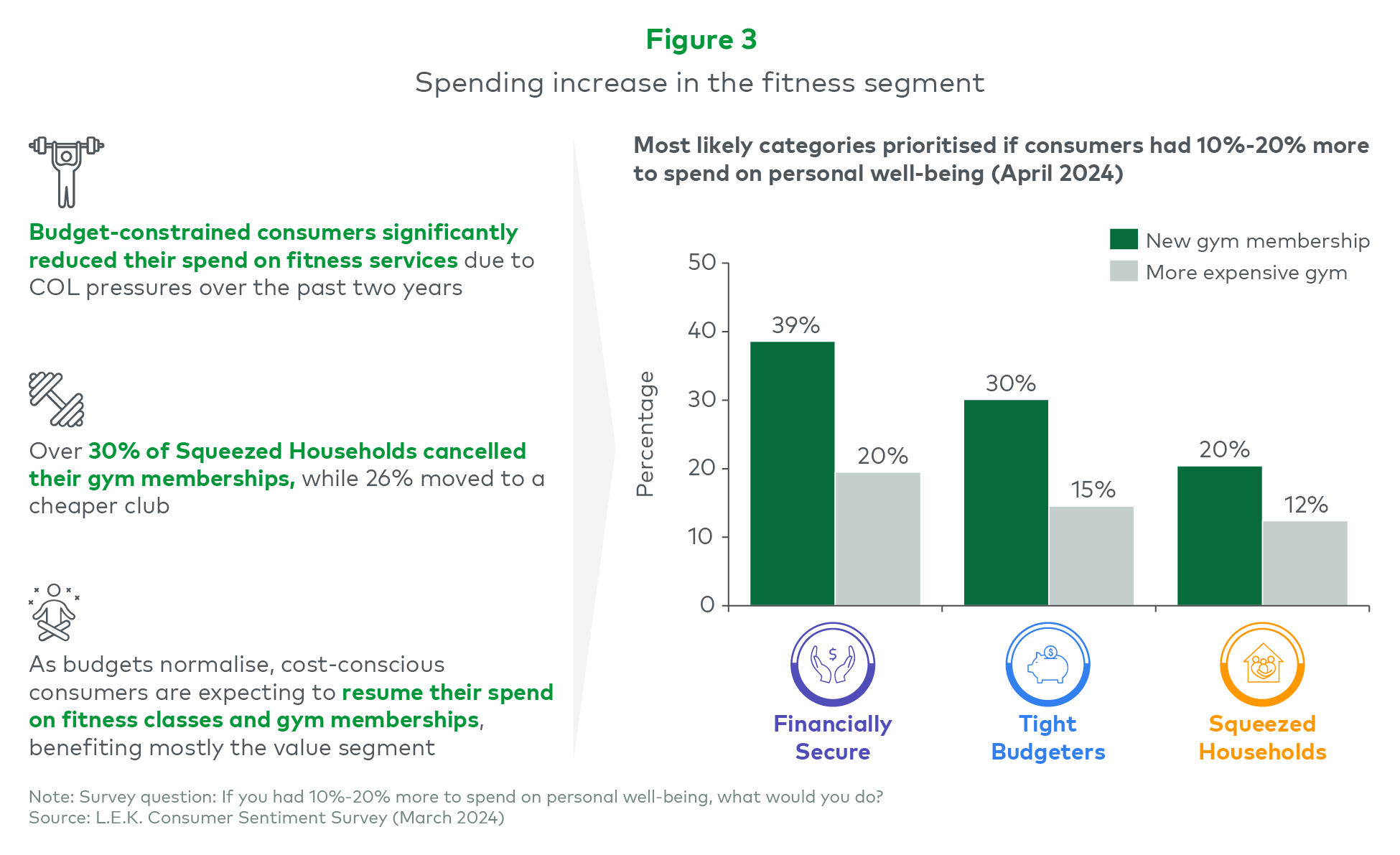

There is also a renewed interest in fitness. The mid-value and value segments in particular appear well-positioned for renewed demand, as more budget-constrained consumers take a refreshed view of expenditure on gym memberships and fitness classes (see Figure 3). Over 30% of Squeezed Households indicated that they have cancelled their gym memberships over the last two to three years while 26% moved to a cheaper club over the last two years. As budgets rebuild and normalise, many of these Squeezed Households have stated that they would be in the market for a new gym membership. Equally 39% of the Financially Secure segment are expected to be looking to enter a new gym membership, though only 20% would be choosing a more expensive membership.

Hospitality trends

Unsurprisingly, consumer spend in UK hospitality venues has been significantly affected by the cost-of-living crisis, with c. 50% of survey respondents reporting a reduction in spending on eating and drinking out. Some parts of the leisure market have also been affected, with 20%-30% of respondents reducing their spending on out-of-home entertainment and live events.

As household budgets improve, hospitality is expected to see a strong recovery in volume terms across consumer segments — with a particular emphasis on casual dining. In addition, there is a positive outlook for entertainment, with 60% of Tight Budgeters and 56% of Squeezed Households indicating they would prioritise live events if they had more to spend on going out with family and friends — potential good news for theatres, festivals, concerts and so on.

Travel trends

Consumer demand for travel has remained strong despite recent cost pressures, with 50% of UK holidaymakers increasing their travel budgets in 2023 relative to pre-pandemic levels. As we move on from the cost-of-living crisis, consumers across all segments expect to increase holiday frequency (64% of Financially Secure and Tight Budgeters stated they will go on holiday more often), whilst 28% of Squeezed Households said they would prioritise international travel.

How L.E.K. can help

The findings of this survey paint a clear picture of UK consumer sentiment in mid-2024, revealing a complex landscape marked by cautious optimism. While some consumers feel their financial situation has improved over the past year, significant worries about energy costs, inflation and mortgage rates persist.

As UK consumers continue to work through these uncertain economic times, there are opportunities for retailers, brands and investors to capitalise on the trends likely to shape the next wave of consumer spending, provided they have a clear understanding of target customer groups and the strategies required to engage them.

To discuss the findings in more detail or to talk about the impact of the trends on your business, please get in touch with Mark Boyd-Boland.

* L.E.K. Consumer Sentiment Survey conducted with 1,000 UK consumers in March-April 2024, covering various age groups, regions and income levels.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting

07032024130739