Key takeaways

-

Specialty beauty retailers like Sephora, drugstores and, most notably, Amazon are increasingly investing in private-label beauty and personal care products.

-

Roughly two-thirds of shoppers believe private label offers great value, with millennials driving the private-label charge.

-

This is creating unprecedented opportunity that extends all the way down the value chain.

-

In this Executive Insights, we discuss the private-label phenomenon and what it means for beauty and personal care products makers, packaging companies, ingredients manufacturers, contract manufacturers and other suppliers.

A shift toward private label is underway in the beauty and personal care products category. Spurred by consumer demand for newer, more innovative product selection and a desire to increase their margins, key retailers — not just specialty beauty retailers like Sephora but also drugstores and, most notably, Amazon — are increasingly investing in private-label beauty and personal care products.

Shopping habits are changing as well. Some 67% of shoppers believe that private label offers extremely good value for the money, according to consumer insights firm IRI. Millennials in particular are helping drive the move toward private label. One survey found that millennials buy private-label products at a higher rate — 32% vs. 25% — than do average shoppers.

With this shift to private label comes an unprecedented opportunity for beauty and personal care products makers, and by extension for the packaging companies, ingredients manufacturers, contract manufacturers and other suppliers that sell to them.

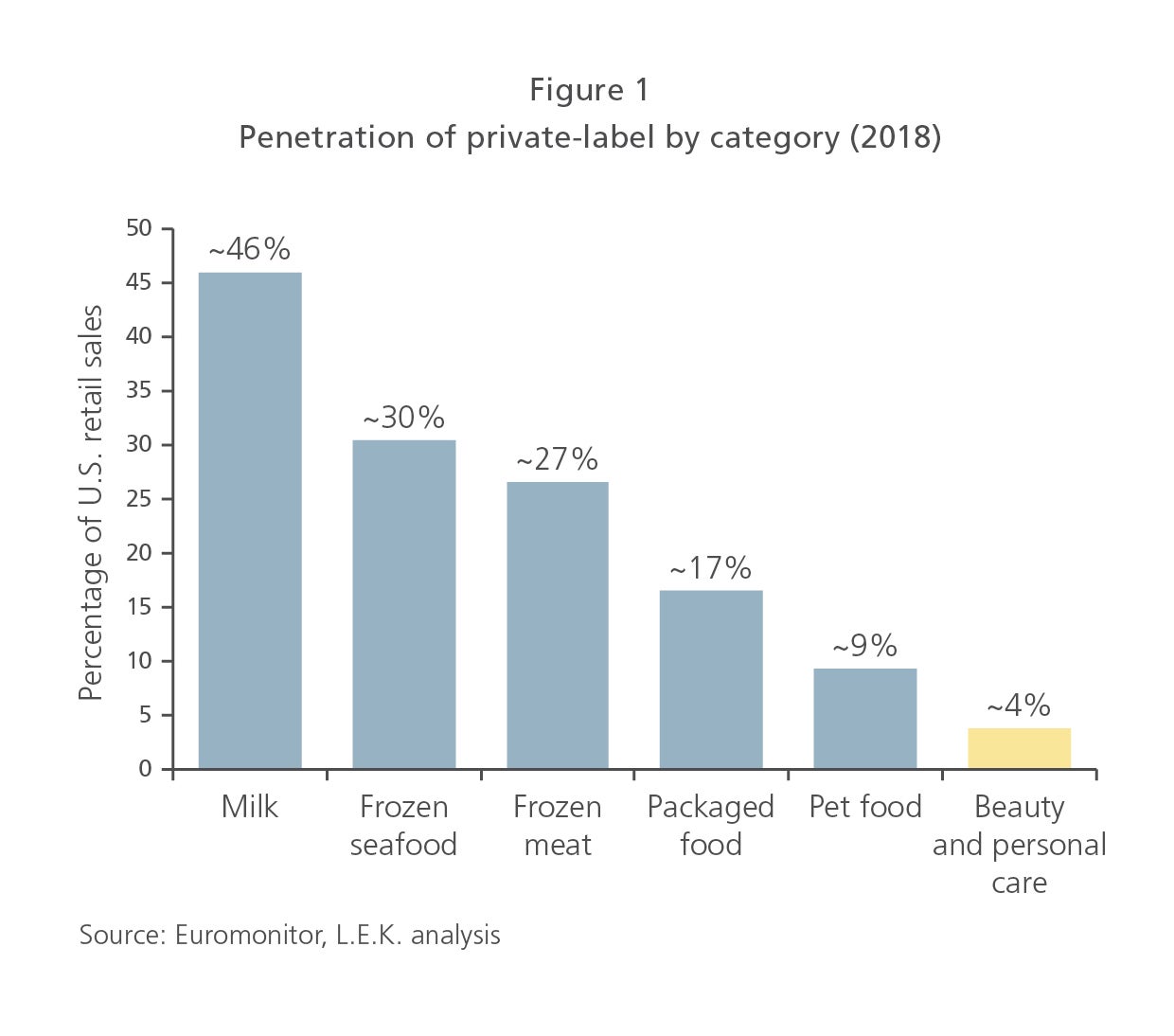

Private-label penetration

Moreover, since 2012, private-label penetration in beauty and personal care products has been relatively stagnant. That's after increasing during the postrecession years, from 3.3% of all spending in the category in 2009 to 4.4% in 2012, according to market research firm Euromonitor. Indeed, consumers often shift toward private-label brands during a recession, and many continue to stick with those brands even after the recession has ended.

However, in some beauty and personal care categories, private label has reverted back toward penetration levels from prior to the last recession, indicating that such offerings could be made more compelling to consumers than they currently are. For example, private-label penetration for bath and shower products was 6.1% in 2018 vs. 7.6% in 2012. In skin care, it was 2.6% in 2018 vs. 3.4% in 2012.

There have been some notable pockets of growth in private-label beauty and personal care products recently. Growth of private-label baby care products has outpaced that of branded products in the past two years, for example, while the growth of private-label men's grooming products has surpassed that of branded products in that category for the past five years. Meanwhile, the comparatively high level of private-label penetration outside beauty and personal care products demonstrates just how comfortable consumers are with nonbranded products.

Retailer investments

Retailers are helping drive this trend toward private label. Specialty beauty retailers like Sephora and Ulta are continuing to invest in private-label products, and drugstores such as CVS and Walgreens are continuing to develop and grow their lines of in-house mass and masstige brands across product segments. Meanwhile, Amazon in March 2019 launched its own private-label line of skin care products called Belei (see Figure 2). The Belei line comprises 12 different items ― such as moisturizers, masks and facial wipes ― that are priced between $9 and $40 and available via Amazon Prime two-day shipping.

But retailers aren't just offering private-label beauty and personal care products at the lowest possible price point. They're expanding and segmenting their private-label offerings, making it clear that, just like with branded items, not all private-label products are created equal. The Walgreens Boots Alliance, for example, is selling a private-label, plant-based beauty and skin care line called Botanics, along with a trendy color cosmetics brand known as CYO and an innovative private-label skin care line dubbed No7.

The burgeoning opportunity

Private-label brands are good investments for retailers, allowing them to preserve margins, offer exclusive products and maintain control of product placement in their stores. But the opportunity that those growing investments retailers are making in private-label beauty and personal care products extends all the way down the value chain. Consumer demand for products that are more natural or innovative can be met by private-label manufacturers, especially when branded manufacturers come up short ― as can a broader expectation of continuously new product options, which is as necessary in the private-label sector as it to branded products. According to a recent L.E.K. Consulting survey, private-label marketing managers expect to increase their SKU counts by 17% over the next two years.

Packaging companies are also well positioned to benefit from this trend toward private label. According to that same survey, private-label brand owners plan to spend more money on packaging over the next year than will branded brand owners. Such investment plans prove that private label is more than just a value price point play, but rather a category that retailers and other value chain participants are working to premiumize.

Indeed, the private-label beauty and personal care products category is ripe for acceleration due to underlying consumer acceptance and retailer investment. As consumer demand for private-label products continues to pick up speed and retailers increase their investments accordingly, beauty and personal care products makers, packaging companies, ingredients manufacturers, contract manufacturers and other suppliers should also be increasing their investments to meet the opportunity that this burgeoning sector presents.

01052021090107