B2C pricing in European healthcare has not been particularly sophisticated historically, and for good reasons. As the markets shift towards more out-of-pocket pay (OOP), and in the current inflationary environment, providers increasingly need to ensure they are pricing competitively. As patients are self-paying, expectations are higher than before, and pricing is a key component of the value proposition.

Effective pricing in healthcare services has been a challenge in Europe historically, given the following factors:

Complicated funding mix and lack of B2C pricing expertise

Healthcare services in many European countries have traditionally been funded either publicly or by private insurance, and pricing for these payers is typically by with tariff, via a tendering process or business-to-business (B2B) negotiations. This is an entirely different approach to pricing for OOP payments, where the view from consumers (on perception, preference and affordability) are contributing factors.

Country-specific regulations

Payers in each country have specific reimbursement structures (particularly relevant for public and insurance payers) and preferences (e.g. preference for bundled prices). Several geographies also have tariffs in place, regardless of the source of funding. Depending on local country regulations, the ‘wiggle room’ for creativity in pricing can therefore vary.

Lack of pricing transparency

Healthcare pricing has historically been inconsistent and not well-documented, particularly in fragmented markets where individual/small clinics often provide variable rates to patients based on relationships. Moreover, in relatively immature markets, pricing data availability is limited. This has made price benchmarking tricky for providers who want to introduce pricing discipline at scale. However, with increased relevance of digital channels and the growing need for transparency (often imposed by regulators), providers have increasingly started publishing prices on their websites, making benchmarking easier than before.

The right pricing strategy

More recently, many of the European healthcare markets are seeing a rise in OOP payments, and that, coupled with the need to pass on inflation, has made it imperative for healthcare providers to build a rigorous approach to pricing across their networks. It is more important now than ever to have a well-thought-out pricing strategy due to factors outlined below:

Growing OOP and B2C aspects

Many healthcare systems in Europe are experiencing increased OOP expenditure driven by constrained public health systems, increased importance of preventive health and higher priority given to healthcare needs post-COVID. This can be seen both in regular healthcare interactions such as with dentists, GPs and ophthalmologists, as well as one-off secondary care such as hip and knee replacements. As patients become payers (and consumers) of the healthcare services, expectations and demand are higher than before, making pricing a key element of the value proposition.

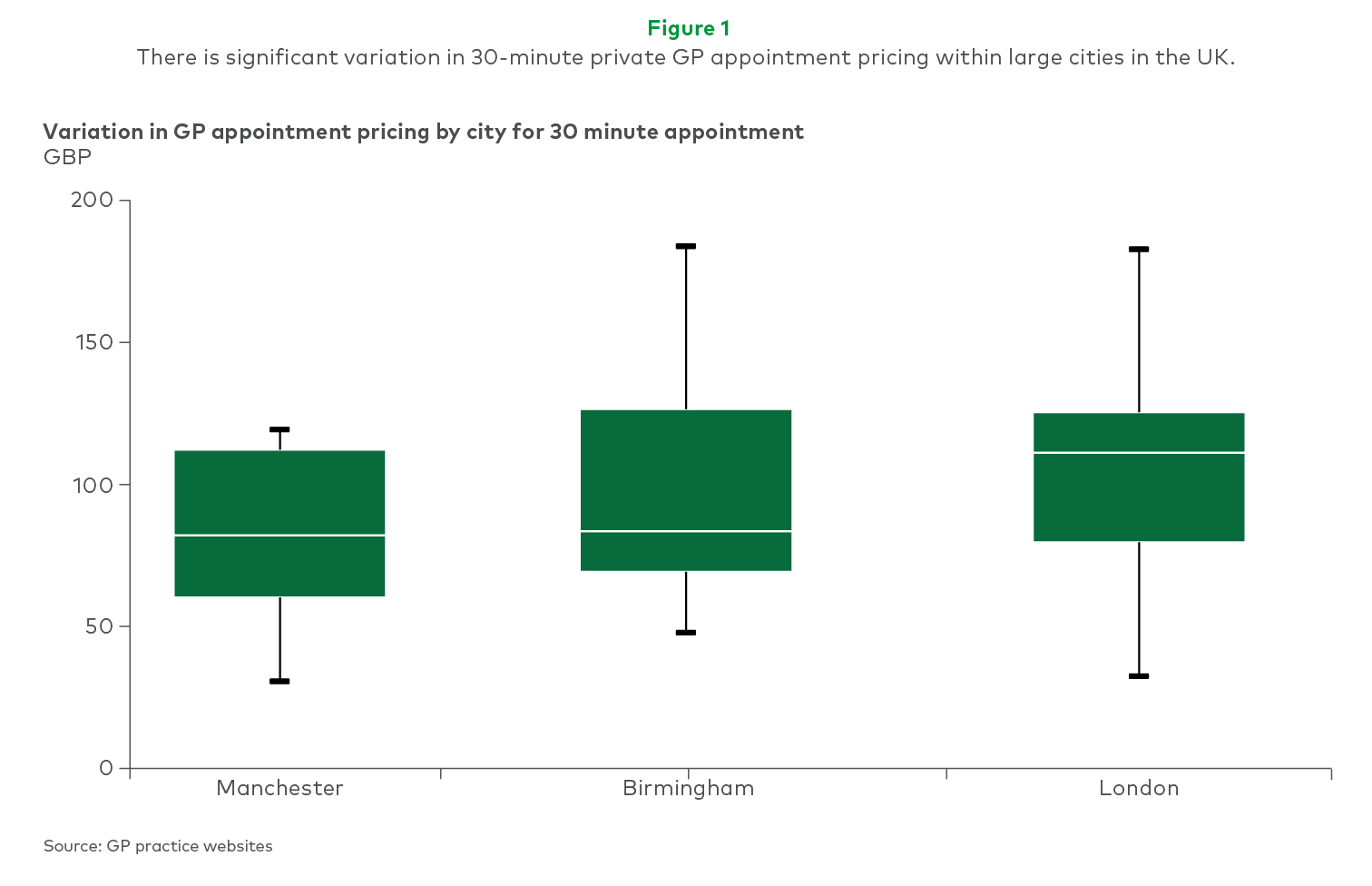

Given the increasing prevalence of self-pay in healthcare services, pricing has become an important value driver; however, services and procedures are still often priced inefficiently, as evidenced by significant price discrepancy across providers in the same location. For example, a 15-minute GP appointment in London for five mid-range private GP providers ranged anywhere from £80 to £180 (see Figure 1).

Increasing competition

Competition is increasing as more players want to address the growing private pay segment than in the past. Some networks are deploying sophisticated pricing mechanisms across their footprint to generate optimum value for the portfolio, creating vulnerability for those who are not.

Cost inflation

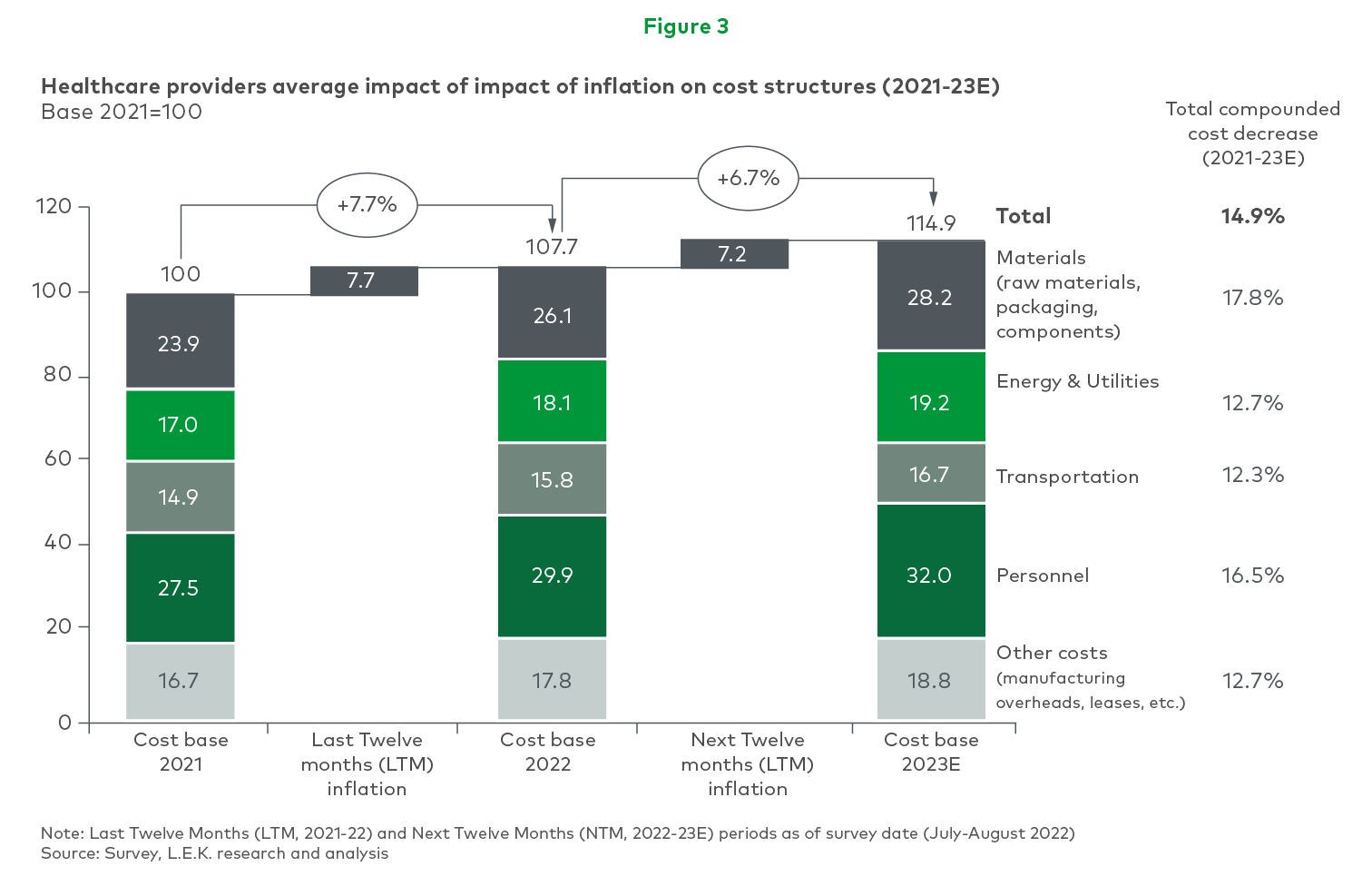

Healthcare providers are experiencing cost inflation due to the increase in costs of material (e.g. dental implants), a significant shortage of healthcare professionals, wage increases and a sharp increase in costs of borrowing and interest on existing corporate debt (see Figure 3).

Quick wins for healthcare providers

Healthcare providers are leaving significant value on the table by not unleashing the power of a well-thought-out pricing strategy. Some quick wins that can be activated include:

Mapping of customer willingness to pay vs. existing pricing structures

Often patients’ need for access and quality is high and they are willing to pay more for the brand and service they value. Identifying these gaps to optimise pricing within the network is an important lever.

Inconsistency across the network

Large networks that do not centralise pricing decision-making often discover significant pricing inconsistencies across the portfolio (even after allowing for varying demographics and income levels by catchment). Learnings from the best practices within the network are key in creating a blueprint for an effective pricing strategy.

Premium for convenience

While the underlying quality of clinical services should remain the same across patient groups, there is potential to create differential, higher-value services for different levels of service/quality, convenience/hours of access. Differential pricing in healthcare is rarely deployed to date.

Pricing as a marketing tool/to promote uptake

Pricing also becomes an important tool to drive uptake of new services/solutions and to create brand awareness in a new market. The balance between attracting a new patient base vs. creating a low-churn, long-standing patient base depends on how the initial and subsequent pricing/discounting strategies are rolled out.

When it comes to increasing profitability, pricing is often the most powerful lever an organisation can pull. At L.E.K. Consulting we have deep experience helping clients define pricing strategies that support their value proposition. We deploy a combination of data analytics and market insights-based tools to create tailored yet scalable pricing strategies for you.

To discuss your pricing strategy, contact L.E.K. Partner Katya Zubareva.

03202023110339